In today’s fast-paced financial world, managing expenses and preparing for future costs is crucial for both individuals and businesses. One effective tool that has been used for decades to manage debt repayment and save for large expenses is the sinking fund. Though its roots lie primarily in the corporate and government bond markets, sinking funds are increasingly recognized as a practical strategy for personal finance as well. This article explores what a sinking fund is, its benefits, practical applications, and why you should consider incorporating it into your financial planning.

Understanding the Concept of a Sinking Fund

A sinking fund is a dedicated reserve of money set aside over time to pay off a debt, replace an asset, or finance a known future expenditure. Traditionally, corporations use sinking funds to systematically retire bond debt before maturity, reducing credit risk for investors. Similarly, homeowners associations might establish sinking funds to cover long-term maintenance and major repairs on community property.

The principal characteristic of a sinking fund is the planned and continual accumulation of money. Instead of encountering a large, lump-sum payment in the future, the borrower or saver allocates smaller, manageable amounts regularly to avoid financial strain. This disciplined approach provides predictability, reduces uncertainty, and strengthens financial stability.

Practical Example: Corporate Bonds

Consider a company issuing $10 million in bonds with a 10-year maturity. To assure bondholders that the company will meet its repayment commitment, it establishes a sinking fund. The company commits to placing $1 million annually into this fund, which can be invested to earn interest. Over ten years, the sinking fund accumulates sufficient money to repay bondholders at maturity, reducing default risk.

The Role of Sinking Funds in Personal Finance

While sinking funds originated in the corporate world, individuals have increasingly adopted this strategy for managing their finances. Many personal financial advisors recommend setting up sinking funds for anticipated expenses such as vacations, vehicle replacements, home renovations, or even holiday gifts.

This approach enables individuals to budget and allocate funds methodically, lessening the likelihood of resorting to high-interest debt when expenses arise. Using sinking funds encourages a proactive mindset towards money management and financial goal-setting.

Real-World Case Study: Home Repairs

John, a homeowner, knows his roof will likely need replacing in the next five years at an estimated cost of $8,000. Instead of facing this large expense all at once, John starts a sinking fund, depositing approximately $134 per month ($8,000 ÷ 60 months) into a high-yield savings account. When the time comes, he has the funds ready, avoiding the need for costly loans or credit card debt.

Advantages of Using a Sinking Fund

There are several compelling reasons to incorporate sinking funds into your financial toolkit. Below are key benefits supported by data and practical insight.

Reduce Financial Stress and Avoid Debt

Unexpected large expenses often lead individuals to take on costly debt. According to a 2023 survey by the Federal Reserve, 40% of Americans would struggle to cover a $400 emergency expense. A sinking fund reduces this vulnerability by building a cash cushion for planned expenses.

By putting aside a fixed amount monthly, you avoid the stress of scrambling for funds when large bills arise. This gradual approach aligns with the principles of sound financial planning and debt avoidance.

Improved Budgeting and Financial Discipline

Sinking funds encourage disciplined saving by dividing future costs into manageable monthly amounts. This method promotes better monthly budgeting and prevents spending impulses. Behavioral economics highlights the effectiveness of “mental accounting,” and sinking funds create designated “accounts” for specific goals, enhancing saving behaviors.

A study by the National Endowment for Financial Education (NEFE) found that regular savers are 30% more likely to reach their financial goals. Implementing sinking funds can be a major contributor to this success.

Protection Against Interest Costs

Taking loans or using credit cards for large expenses often results in high-interest charges. For example, average credit card APRs in 2024 hover around 17%. In contrast, parking money in a low-risk savings or money market account through a sinking fund can reduce or eliminate interest costs altogether.

By avoiding interest payments, you retain more of your hard-earned money, which can be redirected towards investments or other financial priorities.

How to Establish and Manage a Sinking Fund

Creating a sinking fund is straightforward but requires planning and discipline.

Step 1: Identify Your Financial Goal

Begin by pinpointing the specific expense or debt you want to pay down. This could be a planned vacation, new appliance, education fees, or debt repayment.

Step 2: Estimate the Cost and Timeline

Calculate how much money is needed and when you will need it. Try to be realistic and account for potential cost increases, such as inflation or price volatility.

Step 3: Determine the Monthly Contribution

Divide the total amount by the number of months until payment. This monthly target should be incorporated into your monthly budget.

Step 4: Choose the Right Account

Select an appropriate savings vehicle. For short-term sinking funds (under one year), a high-yield savings account or money market fund offers liquidity and decent returns. For longer time horizons, Certificates of Deposit (CDs) or low-risk bonds might be suitable.

Step 5: Automate and Track Progress

Set up automatic transfers to ensure consistent funding and regularly review the fund’s performance. Adjust contributions if needed due to changes in circumstances or goals.

| Step | Task | Practical Tip |

|---|---|---|

| 1 | Define goal | Be specific about expense or debt |

| 2 | Estimate total cost and timing | Use conservative cost figures |

| 3 | Calculate monthly savings amount | Divide amount evenly over months |

| 4 | Choose savings vehicle | Match vehicle to time horizon |

| 5 | Automate & monitor | Use apps or bank features |

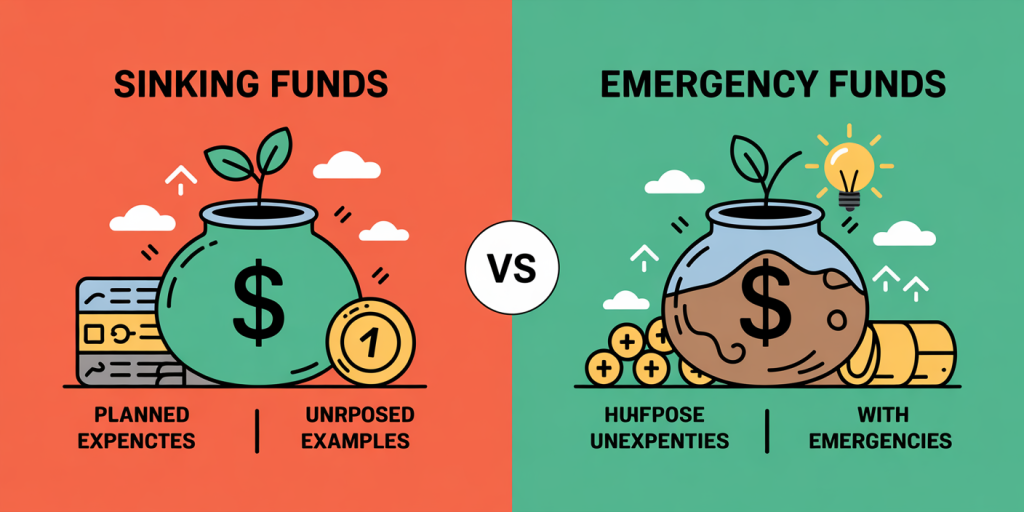

Comparative Overview: Sinking Funds vs Emergency Funds

Many people confuse sinking funds with emergency funds, but they serve different purposes. Below is a direct comparison:

| Feature | Sinking Fund | Emergency Fund |

|---|---|---|

| Purpose | Planned expenses or debt repayment | Unplanned expenses or emergencies |

| Amount | Based on expected cost and timeline | Typically 3-6 months’ living expenses |

| Frequency of Savings | Regular contributions over time | Irregular, as funds are replenished after use |

| Access | Used for specific goal | Used for unexpected financial shocks |

| Examples | Vacation, home repairs, car replacement | Job loss, medical emergency, urgent repairs |

Understanding this distinction helps with more precise financial readiness and overall money management.

Future Perspectives: The Growing Importance of Sinking Funds in Personal Finance

Financial trends suggest that sinking funds will become an even more crucial tool for households worldwide over the next decade.

Increasing Cost of Living and Inflationary Pressures

Rising inflation rates, which averaged around 6.5% annually in 2023 according to the U.S. Bureau of Labor Statistics, have made budgeting more challenging. Prices for goods such as housing, healthcare, and education continue to climb. Sinking funds can help households anticipate and manage these rising expenses by saving gradually.

Expansion of Financial Technology Services

Fintech companies are developing innovative solutions that facilitate automatic saving toward specific goals. Apps like Qapital, Digit, and others now enable users to create multiple sinking funds with automated rules to match spending cycles and income streams. These technologies reduce barriers and enhance saving discipline.

Increasing Financial Literacy and Awareness

Public campaigns and financial education programs globally are promoting tools for long-term financial planning beyond emergency funds and retirement accounts. As awareness increases, sinking funds stand to become a standard feature in personal financial management.

Impacts of Economic Uncertainty

Recent global disruptions, such as the COVID-19 pandemic and supply chain crises, have underscored the value of financial resilience. By compartmentalizing savings through sinking funds, individuals protect themselves from the volatility of unforeseen expenses, thus further cementing its importance.

Practical Takeaways

Modern personal finance demands proactive strategies that balance saving, spending, and debt management. Sinking funds deliver a powerful framework for meeting future expenses without financial strain or resorting to expensive credit. By setting clear goals, planning contributions, and harnessing technology, you can ensure your finances remain stable no matter what costs lie ahead.

With rising economic uncertainties and the increasing cost of living, sinking funds are not just a corporate financial tool but a necessity for individual financial health. Start today by identifying your next large expense, estimating the cost, and opening a dedicated savings account. Over time, the discipline and foresight fostered by sinking funds will not only protect your money but also your peace of mind.

Deixe um comentário